Key Takeaways:

- Financial planning is a structured process that connects your financial life - income, expenses, savings, and investment planning - to reach your goals.

- A comprehensive financial plan includes budgeting, retirement planning, investment strategies, insurance, tax planning, and estate planning.

- Starting early allows compound growth to significantly increase long-term savings.

- Regular reviews help you stay on track and adapt to life changes.

- Professional financial planning services provide financial advice, improve decision-making, reduce costly mistakes and deliver peace of mind.

What is Financial Planning?

Financial planning is the ongoing process of evaluating your financial situation, setting personal and financial goals, and creating a structured plan that includes budgeting, saving, investing, tax planning, and risk management to secure your future financial wellbeing.

Financial planning has never been more relevant – yet it remains widely misunderstood. Too often it is seen as something reserved for the wealthy, the financially sophisticated, or for later life. However in reality it is a practical tool that helps people at every stage make better financial decisions.

At its best, financial planning helps people connect their everyday financial choices with the life they want to build – now and in the future. It brings together everyday money management, protection, long-term saving, and clear goal setting into one joined-up approach. Done well, it helps people feel secure, confident and in control - regardless of income or life stage.

Today, this matters more than ever. Households are navigating rising living costs, economic uncertainty and increasing financial complexity. For many, money is a source of stress rather than security. Increasingly, we are seeing that people who engage in financial planning feel more confident and more in control of their financial future than those who try to manage everything alone, according to Financial Planning Consumer Research, conducted by FPSB in 2023.

That is why financial planning should be seen not as a luxury, but as a life skill — one that belongs to everyone.

Why is Financial Planning Important?

Key Insight: Financial planning creates a clear link between your day-to-day decisions and the future you want to build.

When we talk about financial planning, we are really talking about decision-making. Every day, people make choices that shape their financial future - how they spend, how they save, how they prepare for the unexpected, and how they think about later life.

Without a solid financial plan, these decisions can become reactive. People often move from one financial milestone to the next — starting a career, buying a home, raising a family. Without stepping back, they rarely ask whether their actions align with their longer-term goals.

Financial planning creates that space for reflection. It helps people step back from the day-to-day pressures and ask and ask bigger questions.

- What do I want my future to look like?

- What would financial security mean for me?

- What choices do I want to have in five, ten or twenty years?

The answers are different for everyone, which is precisely why financial planning is so personal.

What is Included in a Financial Plan?

Key Insight: A comprehensive financial plan integrates cash flow management, savings and investments, retirement planning, risk management, tax planning and estate planning into one structured approach.

If you want to create a financial plan that’s practical, it helps to think in terms of building blocks. These components work best when they’re connected, so your money decisions support your full financial picture rather than just one goal.

Budgeting and Cash Flow Management

One of the most common misconceptions is that financial planning starts with investments or pensions. In reality, it often begins much closer to home — with understanding cash flow and budgeting.

Knowing what comes in, what goes out and why is the foundation of good financial wellbeing. It is not about restricting enjoyment; it’s about aligning spending with priorities.

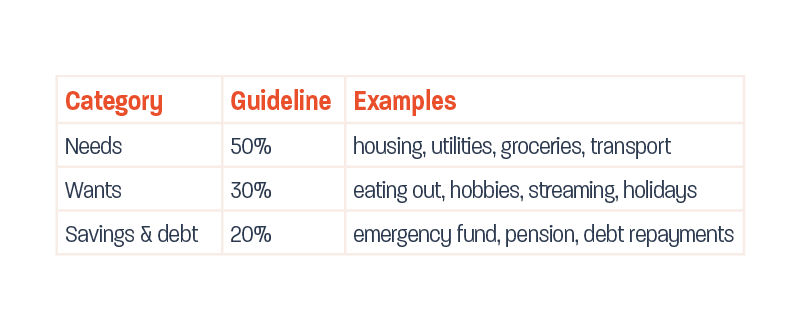

The 50-30-20 method

One simple framework many people find useful is the 50-30-20 approach:

When people become more aware of these patterns, financial decisions start to feel intentional rather than automatic. Saving becomes purposeful, spending becomes more conscious, and financial stress often begins to ease simply because there is a sense of control.

Goal Setting and Prioritisation

Once you understand cash flow planning naturally moves toward setting goals. Clear goals help you decide what matters most right now- and what can wait.

- For a young professional, this might mean balancing rent with starting pension contributions early.

- For a growing family, it may involve managing day-to-day costs while protecting longer-term education or mortgage goals.

- For others, it may mean creating the confidence to change career direction or reduce working hours later in life.

Whatever the goal, planning provides structure – not restriction, but direction.

Insurance Planning

Equally important is insurance planning. Financial planning is not only about growth; it is about resilience. Income protection, life cover and emergency savings help ensure that unexpected events do not undo years of progress. Good financial planning recognises uncertainty and prepares for it.

Retirement Planing

One of the greatest strengths of financial planning involves connecting the present with the future. It recognises that life is lived today, but decisions made today shape the choices available tomorrow.

Retirement planning is a clear example. For many people, retirement feels distant, something that belongs to a future version of themselves. Yet the choices made early — how much is saved, how consistently, and how long those savings have to grow through the power of compound growth — can have a profound difference later on. This is why many people aim to save for retirement steadily, even in small amounts at first.

In Ireland, retirement provision typically combines workplace (occupational) pensions, Personal Retirement Savings Accounts (PRSAs), auto-enrolment and the State Pension. But retirement planning is not simply about pensions.It is about freedom of choice - when to slow down, how to spend time, and how to maintain independence.

The Financial Planning Process Step-by-Step

A structured process makes financial planning easier to follow-and easier to maintain over time. Whether you do it yourself or with a professional, the same steps apply.

Step 1: Assess Your Current Financial Situation Start with a clear picture of where you are today:

- Income (regular and irregular)

- Spending (fixed and variable)

- Debts (including interest rates)

- Assets (cash, investments, property)

- Existing protections (insurance, benefits)

Step 2: Think About Your Long-Term Financial Goals List your goals by timeline:

- Short term (0–2 years): emergency fund, debt payoff, holiday fund

- Medium term (2–7 years): home deposit, education costs, career break

- Long term (7+ years): retirement, long-term investing, legacy planning

Step 3: Choose a Tool, System and/or Automation Consistency matters more than complexity. Choose a system that you’ll actually use:

- Budgeting app or spreadsheet

- Banking alerts (low balance, bill reminders)

- Automatic transfers on payday

- Calendar reminders for quarterly/annual reviews

Step 4: Develop a personalised financial plan - turn goals into action steps, such as:

- Budget adjustments (reduce one cost, set a spending cap)

- Savings targets (weekly/monthly transfers)

- Investing approach aligned to time horizon and risk tolerance

- Retirement contributions

- Insurance updates and emergency fund milestones

Step 5: Monitor and Update Review your plan

If you invest, you might check performance quarterly, but avoid reacting to short-term headlines when your long-term goals haven’t changed.

Common Financial Planning Mistakes and How to Avoid Them

Even with the best intentions, it is easy to fall into financial traps.

People sometimes focus only on growth while overlooking risk management, leaving themselves exposed if circumstances change.

Others create a plan but fail to revisit it as life evolves or react emotionally to short-term market movements. Over time, over-reliance on debt or reacting to headlines rather than long-term goals can quietly erode financial security.

A well-structured plan acts as a set of guardrails, helping people stay disciplined and focused during periods of uncertainty.

What are the advantages of Professional Financial Planning vs. DIY Approach?

We live in a time when financial information is everywhere. Podcasts, social media, online tools and apps have made financial content more accessible than ever – which is positive. Yet access to information does not always translate into clarity.

Increasingly, the challenge is not finding information but knowing how to apply it to real life. Financial decisions are deeply personal and often emotional. What works in theory or for someone else may not suit an individual’s own circumstances.

This is where professional financial planning can add real value. A skilled financial planner helps turn information into insight, bringing perspective, structure and objectivity. Professional guidance is not about taking control away from individuals. It is about helping them make better decisions with confidence and stay focused on what matters most— their goals, values and quality of life .

2026 Trends in Financial Planning

Technology and Fintech InnovationFinancial planning itself continues to evolve. Technology is changing how people engage with their money, making planning more accessible, more transparent and more connected to everyday life. Digital tools help people track progress and stay organised, while face-to-face relationships continue to provide the human insight and reassurance many still value.

Financial Planning for Diverse Incomes and Lifestyles

At the same time, financial lives are becoming more diverse. Career paths are less linear, families are more varied, and people are living longer and redefining what retirement looks like. Financial planning must continue to adapt to these realities — moving away from one-size-fits-all assumptions and toward more personalised, flexible approaches.

What remains constant is the need for guidance that helps people make sense of complexity.

Conclusion

Financial planning about creating a framework that allows people to move forward with confidence, knowing their decisions align with what matters most.

Ultimately, financial planning is not about chasing perfection or predicting the future. It is about giving people clarity and choice — the ability to make decisions today that support the life they want tomorrow. And that is why financial planning should be seen as an essential part of financial wellbeing for everyone.

FAQs:

Financial planning is the process of understanding your money and making a clear plan for how to use it to support your goals. It connects your income, spending, saving, and investing decisions so they work together — not separately — to build financial security over time.

Yes. Financial planning is not just for high earners or people with large investments. It’s a practical life skill that helps anyone — regardless of income — make better financial decisions, reduce stress, and feel more in control of their future.

The best time to start is as early as possible — even if you can only save small amounts at first. Starting early allows compound growth to work in your favour, meaning your money has more time to grow. But it’s never too late to begin; financial planning can add clarity at any stage of life.

A basic financial plan typically covers:

- Budgeting and cash flow management

- Saving and emergency funds

- Retirement planning

- Investment strategy

- Insurance and protection

- Tax and estate planning

Many people start with DIY tools such as budgeting apps or spreadsheets. However, professional financial planning can provide structured guidance, objective advice, and help avoid costly mistakes. The right choice depends on your confidence, complexity of needs, and personal preference.

Author –

Emer Kirk, CEO, Financial Planning Standards Board